kebatex

India

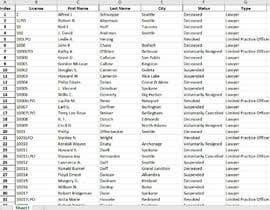

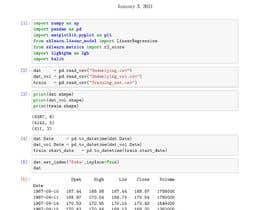

Develop a ML/AI model to predict result of trades. Value to be predicted shown in training data first column "result" (response variable). Underlying data and volatility shown in separate files. The underlying and volatility data are two time series to be used to predict the result. (You can use any other market data that you feel fit as well)

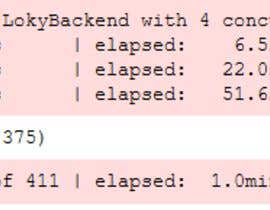

R2 is to be computed as leave-one-out cross validation (k-fold cross validation with number of folds equal to number of values). Please post this value to your entry (highest one is the winner). Please include code and results in your pdf file clearly showing your method, the leave-one-out prediction result for each value in the "results" column of the training set, your feature generation method (if applicable) and the overall R2. I should be able to replicate your method and verify your results from your document.

Data to be used for prediction is time-series in nature (as showing in the two underlying files), so CANNOT use any data after trade date (shown as start date column in training data) for prediction. Entries using any data from dates after trade date are not eligible.

Those with strong entries may be contracted for additional tasks.

Prize guaranteed.

Post Your Contest Quick and easy

Get Tons of Entries From around the world

Award the best entry Download the files - Easy!